What is stablecoin infrastructure

As stablecoin transaction volumes have surpassed those of major card networks and the GENIUS Act has established a federal regulatory framework in the US, this infrastructure is quickly becoming the operational backbone for cross-border payments, treasury management, and embedded finance. For teams evaluating this space, understanding how each layer works determines how fast you can move, where you can operate, and what you can offer your customers.

Below, you'll learn what makes up the stablecoin infrastructure stack, how each layer works in practice, how settlement times compare across chains and fiat rails, what compliance looks like after the GENIUS Act, how private blockchains fit into the picture, and what to evaluate when choosing an infrastructure provider.

What's in this article?

- How does stablecoin infrastructure differ from traditional payment infrastructure?

- What are the layers of the stablecoin infrastructure stack?

- How do onramps and offramps work in practice?

- How does stablecoin settlement compare to traditional payment rails?

- How does privacy fit into stablecoin infrastructure?

- What should fintech teams evaluate when choosing stablecoin infrastructure?

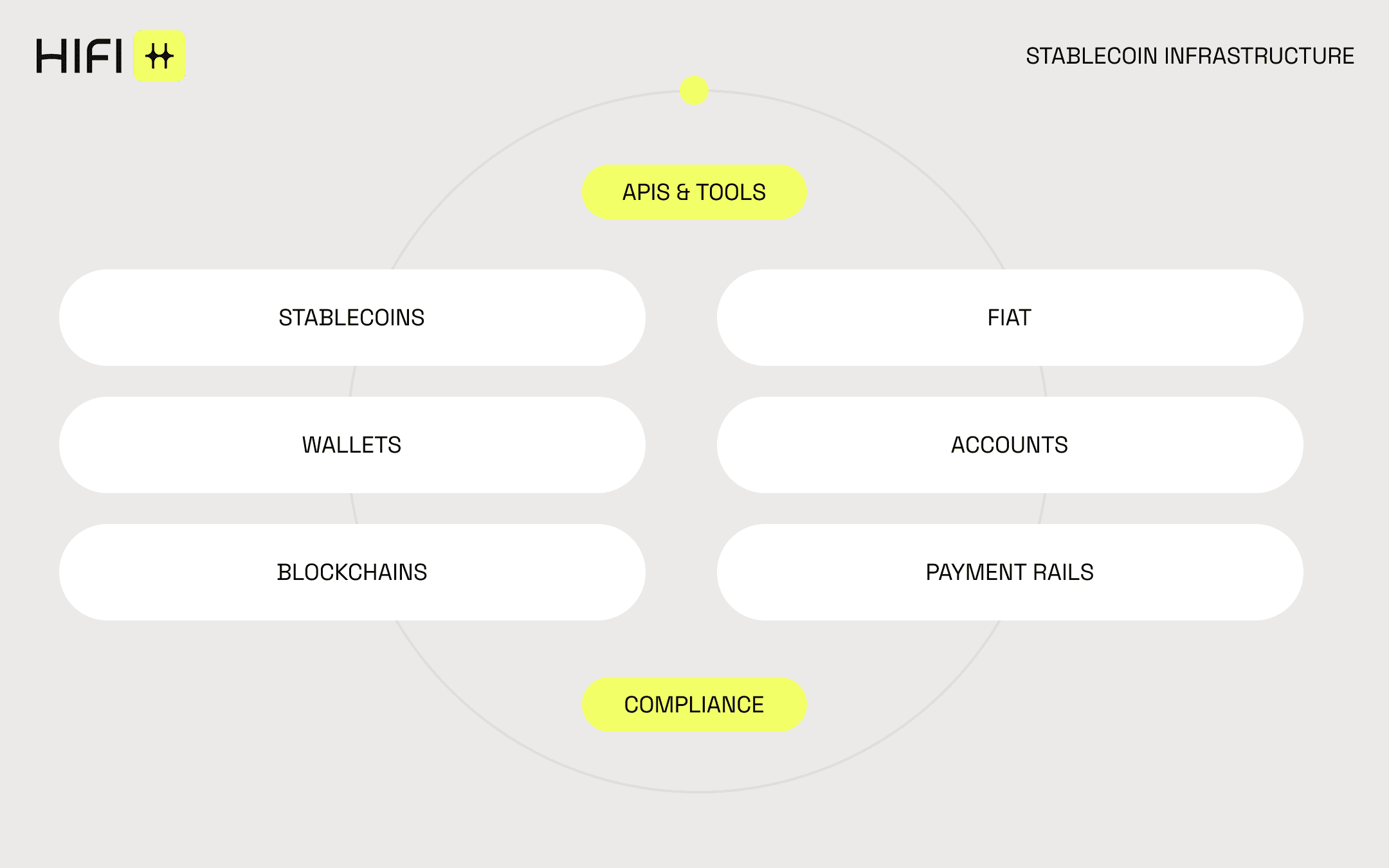

What are the layers of the stablecoin infrastructure stack?

Traditional payment infrastructure handles card networks, ACH transfers, and wire systems. Stablecoin infrastructure builds on top of this, integrating blockchain networks alongside traditional rails to enable faster settlement, programmable money movement, and direct access to global corridors.

Rather than building direct integrations with each blockchain, each bank, and each compliance provider, businesses plug into infrastructure that abstracts that complexity into APIs, wallets, and routing logic.

Stablecoin infrastructure is a stack of interconnected layers, each handling a distinct responsibility.

Blockchain networks

Blockchain networks are where stablecoins are issued, transferred, and settled. This is the base layer that every other part of the onchain stack depends on.

The choice of network depends on more than speed and cost. Liquidity depth, institutional familiarity, privacy capabilities, decentralization guarantees, ecosystem maturity, and regional adoption patterns all factor into the decision. Ethereum carries deep liquidity and broad institutional trust, which is why it remains the default for large-value settlement despite higher fees and slower confirmation times. Solana settles in fractions of a second at lower cost, making it a fit for high-frequency, lower-value flows. Tron handles a large share of global USDT volume, particularly in Asia, where its network effects and low fees have made it the de facto rail for peer-to-peer stablecoin transfers. Layer-2 networks like Base, Arbitrum, and Polygon inherit Ethereum's security model while reducing cost and latency. And private networks like Canton serve institutions that need onchain settlement without public transaction visibility

Most stablecoin infrastructure platforms today support multiple chains to acommodate for diverse developer needs across userbase, trust, and cost.

Wallet and custody infrastructure

Wallets and custody systems determine how stablecoin value is held, who controls access, and how funds move in and out of the stack.

Custodial wallets are managed by an infrastructure provider, meaning the business or platform holds the keys on behalf of its users. This is the most common model for consumer-facing products where simplicity and control over fund flows matter more than user-level key management.

Non-custodial wallets give users direct control of their own keys, removing the provider as an intermediary. This model appeals to crypto-native teams and developers who want to minimize counterparty risk or build on top of open wallet standards.

Modern wallet infrastructure handles key management, transaction signing, and embedded wallet provisioning at the API level. A business can spin up a wallet for each end user programmatically, without the user ever interacting with blockchain mechanics directly.

Fiat onramps and offramps

Onramps convert traditional currency into stablecoins. A business deposits USD via ACH, wire, or real-time payments, and receives stablecoins in a wallet. Offramps do the reverse, converting stablecoins back into local currency and delivering funds through bank transfers, local payment rails, or mobile money.

Stablecoin infrastructure connects onchain needs to banking realities. Effective onramp and offramp systems integrate with banking partners, handle identity verification during the conversion process, and support multiple payout methods across different countries.

Compliance and identity tooling

Any infrastructure that moves money needs to handle Know Your Customer (KYC) verification, Know Your Business (KYB) checks, anti-money laundering (AML) screening, sanctions monitoring, and transaction-level reporting. With the US GENIUS Act establishing a federal framework for dollar-backed stablecoins, these capabilities have moved from nice-to-have to baseline infrastructure requirement.

Speed matters here. Programmatic KYC that resolves in under two minutes is a fundamentally different builder experience than manual review queues that take days. For businesses onboarding users at scale, the difference directly affects conversion rates and time to revenue. The strongest infrastructure providers embed compliance directly into the payment flow — transaction monitoring, sanctions screening, and suspicious activity reporting run automatically — rather than requiring businesses to layer in separate tooling.

Orchestration

Orchestration is the coordination layer that sits above chains and rails. Stablecoins exist on multiple blockchains. Fiat moves through dozens of different payment systems. Compliance requirements vary by corridor. Exchange rates shift. Without something coordinating all of this, every business would need to build its own routing logic, manage cross-chain liquidity, and maintain separate integrations for each rail.

An orchestration layer connects blockchain networks and banking rails into a single interface, routing transfers across the most efficient chain, managing asset conversions, and applying programmable logic at the transaction level. Fee collection, settlement timing, batch payouts, and multi-party approvals are all coordinated at the orchestration layer.

For a fintech building a remittance product, orchestration means supporting payouts to dozens of countries through their local rails — PIX in Brazil, SPEI in Mexico, mobile money across Sub-Saharan Africa — from the same API, without separate integrations for each. For a marketplace, it means settling payments to global sellers in their preferred currency while collecting platform fees automatically on every transaction.

APIs and developer tools

APIs and developer tools are how developers interact with the stack, exposing every operation from wallet provisioning to transfers to compliance checks through a single integration surface. REST endpoints collapse every operation — user creation, wallet provisioning, KYC, transfers, onramps, offramps, swaps — into one API. Webhooks enable real-time event notifications, sandbox environments for testing, and comprehensive documentation.

The developer experience determines how quickly a team can go from idea to production.

How do onramps and offramps work in practice?

Onramps convert fiat currency into stablecoins, and offramps convert stablecoins back into fiat. Together, they're the entry and exit points between traditional money and blockchain-based payments.

The simplest way to understand onramps and offramps is to follow a payment through the system.

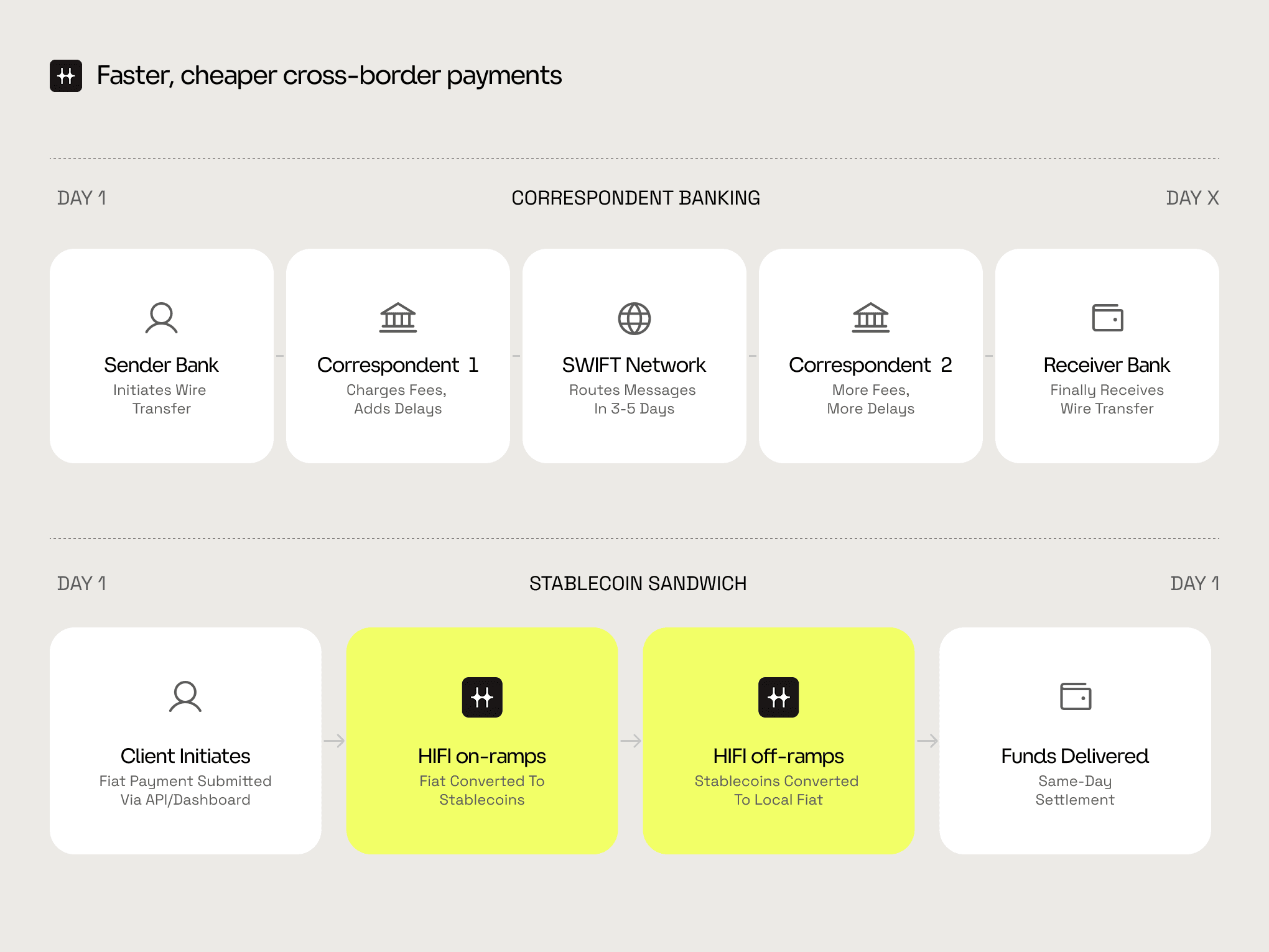

A US-based business needs to pay a contractor in Brazil. The business deposits USD into a virtual account via ACH or real-time payment. The onramp converts that deposit into USDC, and sends the money onchain to the contractor's wallet, where an offramp converts it to BRL and delivers funds via PIX, Brazil's instant payment rail.

What would traditionally take two to three days through correspondent banking with multiple intermediary fees happens in minutes with a single integration. The infrastructure handles the conversion, compliance checks, and last-mile delivery behind the scenes.

The same pattern applies in reverse. A business in Latam receiving payment from a US client can accept local currency, convert it to stablecoins, and hold value in USDC until it's ready to offramp into another currency. Onramps and offramps are the connective tissue between the fiat and blockchain worlds.

How does stablecoin settlement compare to traditional payment rails?

Settlement speed is the most commonly cited advantage of stablecoin infrastructure. But the blockchain leg of a payment — the part that settles in seconds — is rarely the bottleneck. What determines real-world speed is how quickly value moves between fiat and stablecoins: the onramp and the offramp.

Onramp speed: fiat to stablecoins

When a business or end user deposits fiat to convert into stablecoins, the speed depends on which payment method they use to fund the conversion.

| Method | Settlement Time |

|---|---|

| RTP (Real-Time Payments) | Near-instant |

| Wire (domestic US) | Same day if initiated before 3pm ET |

| ACH Same Day | Same business day (cut-off windows apply) |

| ACH Standard | Next business day |

The difference between an onramp that accepts RTP and one that only supports standard ACH is the difference between stablecoins in your wallet in minutes versus tomorrow. For exchanges handling client deposits, fintechs funding virtual accounts, or treasury teams moving capital into stablecoins, onramp speed directly affects how quickly downstream operations can begin.

Offramp speed: stablecoins to local currency

When it's time to convert stablecoins back to fiat and deliver funds, the speed depends on the destination corridor and the local rail available.

| Method | Settlement Time |

|---|---|

| RTP (US domestic) | Near-instant |

| Domestic wire (US) | Same day if initiated before 3pm ET |

| SWIFT (international) | Typically under T+2 |

| PIX (Brazil) | Instant |

| SPEI (Mexico) | Minutes |

| Mobile Money (Sub-Saharan Africa) | Instant to same day |

Infrastructure that can offramp to PIX or mobile money delivers a fundamentally different experience than one limited to SWIFT. For a remittance product paying out to Brazil, that's the difference between funds arriving in seconds and funds arriving in days.

Money moves across blockchains in seconds, but the infrastructure question is what happens on either side of the chain: how fast fiat converts in, and how fast local currency pays out.

How does privacy fit into stablecoin infrastructure?

Most stablecoin infrastructure runs on public blockchains, where every transaction is visible on a shared ledger. Transparency is a feature for many use cases, but it can also be a dealbreaker. A bank settling with a counterparty doesn't want competitors to see the amounts, timing, or parties involved. A corporation rebalancing treasury positions across entities doesn't want that activity on a public ledger.

Privacy solutions in stablecoin infrastructure take different forms. Some networks build privacy in at the protocol layer, where transactions, balances, and contract state are visible only to authorized parties by default. Other blockchains layer privacy tooling on top of public chains, using techniques like zero-knowledge proofs or permissioned execution environments to shield sensitive data while still settling on a shared network.

The use cases for privacy are often institutional: interbank settlement, treasury movements between entities, clearing and payment network settlement, and market-maker flows where confidentiality is a business requirement.

What should fintech teams evaluate when choosing stablecoin infrastructure?

When you're evaluating providers, there are several criteria to consider:

Onramp and offramp speed: How quickly can fiat convert into stablecoins, and how quickly can stablecoins pay out to local currency? Does the provider support RTP or instant payment methods for onramps, or only standard ACH? On the offramp side, can you deliver funds via local rails like PIX or mobile money, or are you limited to SWIFT?

Compliance speed: How long does KYC take? KYB? Is the compliance team in-house, or does the provider outsource to a third-party wrapper?

Privacy capabilities: Can the provider support private settlement for institutional use cases? If you're serving banks, corporate treasuries, or market makers who need to move value onchain without public visibility, the availability of privacy infrastructure matters.

Chain coverage: How many blockchain networks does the provider support in production? Can you add new chains without re-integrating? A provider supporting many chains gives you more routing flexibility than one locked to a single network.

Fiat coverage: What onramp and offramp corridors are live? The more corridors available through a single integration, the less vendor sprawl you manage.

Account architecture: Are virtual accounts named — meaning the sender's and recipient's names appear on transactions — or are they omnibus accounts where the provider's name shows up? Does the platform support both first-party and third-party payments?

White-label capability: Does the provider's brand appear anywhere in the payment flow, or is the infrastructure invisible to end users?

API design and sandbox: Can you test the full integration in sandbox before going live? Are webhooks granular enough to cover each step in the onramp, offramp, and transfer lifecycle? Is the documentation comprehensive, up to date, and written for developers?

HIFI connects blockchain networks to banking and payment rails through a single API. Start in sandbox today or talk to the team to see how it works in production.