Where HIFI Reaches: Global Payout Coverage Across Stablecoins and Local Rails

Software is global on day one, but payments arent. A two-person startup can ship a product to 100 countries on day one. But when it's time to pay a seller in Lagos, a contractor in São Paulo, or a driver in Hong Kong in their local currency, through a rail they can actually access, platforms stall. Moving money remains the hardest part of going global.

HIFI settles stablecoin payouts into local currency across 60+ countries through a single API. Below, you'll learn how HIFI's payout coverage breaks down by region, what rails and currencies are available in each corridor, and how a single integration replaces the multi-partner architecture most teams end up building.

What's in this article?

- Why is building global payout coverage so difficult?

- How does HIFI's SWIFT coverage work across 60+ countries?

- How do stablecoin payouts work in Latin America?

- What Asia-Pacific payout corridors does HIFI support?

- How does US domestic settlement fit into a global payout stack?

- What does one integration across all these rails actually mean?

Why is building global payout coverage so difficult?

A single stablecoin payout from the US to Brazil might seem straightforward: convert USD to USDC, send it onchain, off-ramp into BRL via Pix. But each step requires dedicated infrastructure — a provider to convert fiat into stablecoins, a wallet layer to hold and move tokens onchain, a partner with Brazilian banking access to convert stablecoins back into reais, and a way to deposit those reais into the recipient's account via Pix.

Building that as a product means integrating with an on-ramp provider, a blockchain wallet layer, an off-ramp partner with Brazilian banking access, and a compliance stack that satisfies both US and Brazilian regulators. Add multiple countries to the mix and the stack increases drastically: ACH, SWIFT, RTP, mobile money, and each country’s specific payments system. Each corridor introduces a new provider, a new API surface, and a new set of settlement rules.

This is the multi-provider problem, and it's the default architecture for most fintech teams building global payouts. In practice, it means managing four or five separate integrations — each with its own webhook format, its own error taxonomy, its own settlement schedule, and its own reconciliation output. A SWIFT payout confirms differently than a mobile money transfer in Uganda, which confirms differently than an ACH credit in the US. Matching those confirmations back to a single internal ledger requires custom normalization logic per provider, and that logic has to be maintained every time a provider changes their API.

The compliance overhead scales with the number of partners. Each provider has its own KYC and AML posture, its own onboarding requirements, and its own regulatory footprint. If you're using one provider for US domestic rails and another for Latam off-ramps, you're managing two compliance relationships — two sets of screening rules, two sets of documentation requirements, two sets of regulatory updates to track.

Every payout that settles in local currency requires liquidity in that currency. A payout to Mexico via SPEI requires MXN liquidity, and a payout to Singapore via bank transfer requires SGD liquidity. If each corridor is handled by a different provider, you're pre-funding balances across multiple platforms, fragmenting your treasury and making it harder to forecast cash-flow. The alternative is just-in-time funding, but that requires each provider to support real-time conversion at competitive rates, which not all of them do.

The net result: the integration layer itself becomes the bottleneck. Teams spend more engineering time maintaining provider adapters, reconciliation scripts, and fallback logic than they do building their product. This is the problem an orchestration layer solves: connecting sprawling rails and logic behind a single API that handles routing, conversion, compliance, and reconciliation across every corridor.

How does HIFI's SWIFT coverage work across 60+ countries?

HIFI supports SWIFT payouts to 60+ countries through a single API. The developer specifies the recipient, the destination country, and the target currency, and HIFI handles the routing.

USD SWIFT payouts are live to 31 countries, including the United States, Canada, the UK, Japan, India, the Philippines, Colombia, and major European markets like Germany, France, Italy, Spain, the Netherlands, and the Nordics. These typically clear in under two business days.

For non-US originators and in corridors where recipients need to receive funds in their own currency, HIFI settles in local currency directly. Key corridors include Hong Kong, China, Singapore, Brazil, and Mexico. Each of these is covered in detail in the regional sections below.

How do stablecoin payouts work in Latin America?

Latin America's two highest-volume stablecoin corridors — Brazil and Mexico — are both live on HIFI through the Global Network Rail. The rails are fast, the currencies settle natively, and both corridors represent significant demand from fintechs building remittance, contractor payout, and marketplace disbursement products.

Brazil (BRL via Pix): Pix is Brazil's instant payment system, operated by the Central Bank of Brazil. Since its launch in 2020, Pix has become the dominant settlement method for digital payments in the country, processing billions of transactions annually. HIFI supports BRL payouts via Pix, which means recipients receive Brazilian reais directly in their bank accounts with near-instant settlement. For fintechs building US-to-Brazil remittance flows or paying Brazilian contractors, this eliminates the multi-day settlement and FX overhead of routing through SWIFT.

Mexico (MXN via SPEI): SPEI is Mexico's interbank electronic payment system. HIFI supports MXN payouts through SPEI, delivering Mexican pesos to the recipient's bank account with same-day settlement. Mexico is one of the world's largest remittance corridors, and MXN settlement via SPEI is the expected delivery format for most recipients.

For developers building cross-border payout products, these two corridors cover the bulk of Latam stablecoin demand. A US-based fintech paying contractors in São Paulo and Mexico City can fund in USD, convert to stablecoins, and settle in BRL and MXN through the same API used for SWIFT payouts to Europe and mobile money payouts to Kenya.

"Every fintech team we talk to building Latam payouts tells us the same story: Brazil needs a Pix integration, Mexico needs SPEI, and neither talks to your SWIFT provider. So you end up with three vendors, three compliance relationships, and three pre-funded balances, just to cover two countries. Meanwhile, your recipient in São Paulo just wants reais in their bank account in seconds. The delivery format is part of your product experience, and we think that's a problem worth solving at the infrastructure layer.”

- Zach Walsh, CEO of HIFI

What Asia-Pacific payout corridors does HIFI support?

HIFI's Asia-Pacific coverage is focused on Hong Kong and China, two of the most important corridors for enterprise treasury operations and institutional settlement.

Hong Kong (HKD): Payouts via SWIFT, CHATS (Clearing House Automated Transfer System), and FPS (Faster Payment System). CHATS is Hong Kong's real-time gross settlement system for high-value transactions. FPS handles lower-value, near-instant transfers. Between the two, HIFI covers the full range of payout sizes for businesses operating in Hong Kong.

China (CNY): Payouts via SWIFT. Direct CNY settlement is a rare capability among stablecoin infrastructure providers, and it matters for businesses that need to pay suppliers or partners in mainland China without routing through intermediary currency conversions.

Singapore (SGD): Payouts via local rails. Singapore functions as a financial hub for Southeast Asia, and SGD settlement complements the Hong Kong and China corridors for treasury teams managing regional liquidity.

These corridors are accessible through the same Global Network Rail that handles SWIFT and Latam payouts.

How does US domestic settlement fit into a global payout stack?

If you're building a global payout product, US domestic settlement is essential. But it still has to work well, and the details of which rails are supported, how fast they settle, and what cut-off times apply matter for your product's user experience and your treasury operations.

HIFI supports three domestic USD payout methods:

RTP (Real-Time Payments): Near-instant settlement to eligible US bank accounts, available 24/7. For products where recipients expect to see funds immediately, including gig economy payouts, earned wage access, and real-time marketplace disbursements, RTP offers the fastest domestic payout rail.

ACH: Available in both same-day and standard variants. Same-day ACH settles within the same business day, with cut-off times at 10am, 2pm, and 4pm ET. Standard ACH settles the next business day. ACH is the workhorse rail for high-volume, lower-urgency payouts: payroll, vendor payments, marketplace disbursements, and recurring transfers. It's the highest-volume domestic rail for most HIFI customers.

Wire: Same-day settlement if initiated before 3pm ET; next business day after. Wire is the right rail for high-value, time-sensitive payments where the recipient needs confirmed, irrevocable funds on the same day.

HIFI also supports SWIFT payouts from the US for international delivery, which means a single platform handles both the domestic and cross-border legs of a global payout flow. A developer building a marketplace that pays US-based sellers via ACH and international sellers via SWIFT or Pix can do so through one integration with HIFI.

For moving fiat into stablecoins to fund global payouts, HIFI supports ACH Push, wire, and RTP for USD deposits. Developers on HIFI can mint USDC from a fiat deposit in under 10 minutes during business hours. This means a business can fund its stablecoin treasury and begin executing global payouts within the same session, rather than waiting for overnight settlement before the onchain balance is available.

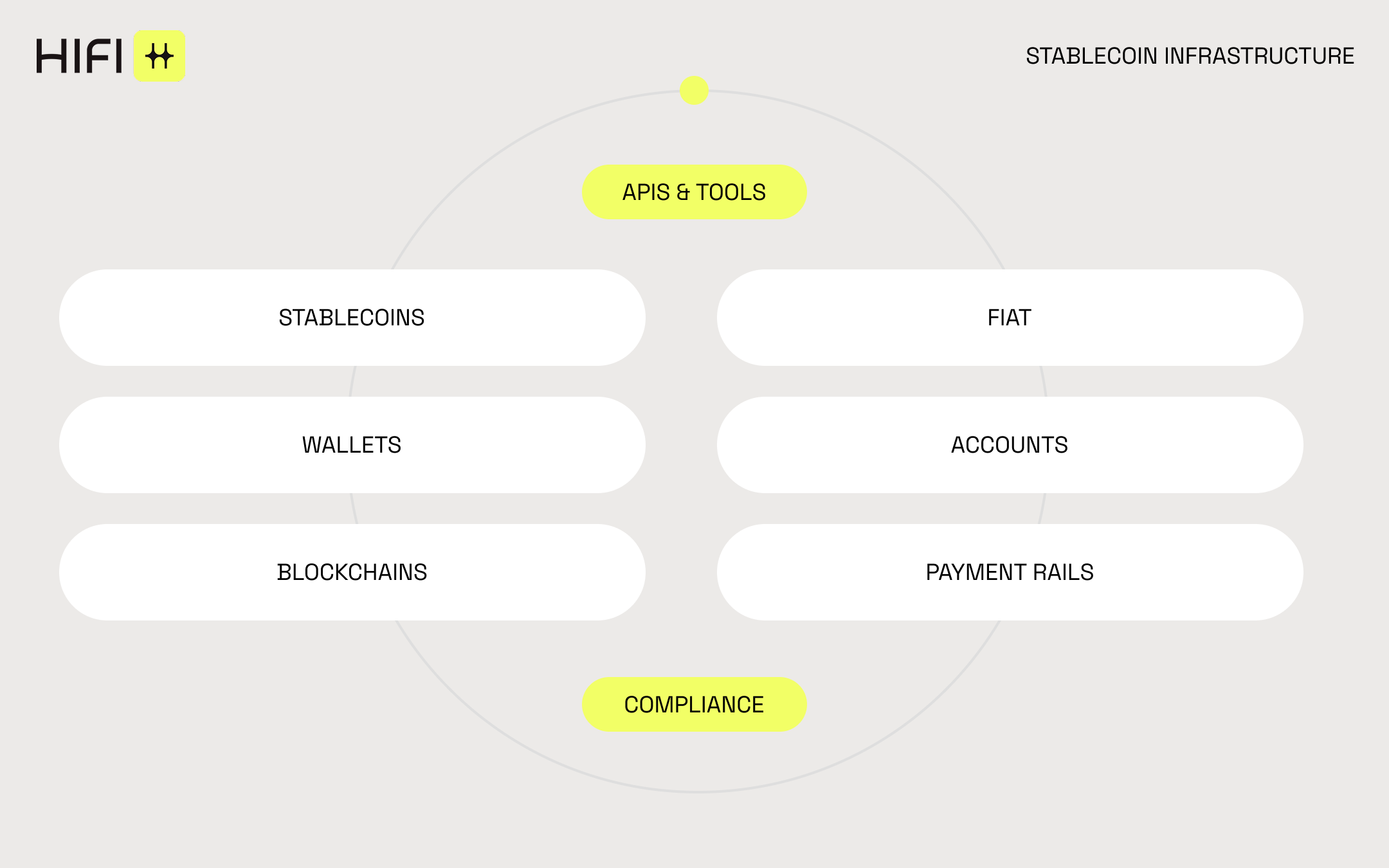

What does one integration across all these rails actually mean?

With HIFI, you can reach 60+ countries across SWIFT, local payment rails, and onchain networks through a single API.

A developer creates an offramp account for each recipient, specifying the destination country, currency, and transfer method. A payout to Hong Kong uses a Global Network account and settles via FPS in Hong Kong dollars. A payout to a US bank account uses a US account and settles via RTP or ACH.

The same applies on the blockchain side. HIFI supports live wallets across every major blockchain network. Stablecoins move between chains and into fiat rails through the same orchestration layer, which means both the onchain and offchain legs of a global payout are handled in one place. Supported stablecoins include USDC, USDT, PYUSD, and USDG, with chain-specific availability documented in the API reference.

Unified compliance means HIFI runs programmatic KYC for individuals and KYB for businesses through an in-house compliance team. Onboarding is designed to be fast and frictionless: most individuals clear compliance in minutes, and businesses are typically approved within a business day. Compliance checks, transaction approvals, and regulatory screenings are embedded into every payout flow regardless of which rail carries the funds.

This is what orchestration means in practice: not a single rail, but a layer that connects everything — blockchains, banking networks, instant payment systems, and mobile money — so developers can build global payout products without assembling the infrastructure themselves.

Explore the docs to see full corridor coverage, or start building in sandbox today.

Related Posts

April 9, 2026

April 9, 2026What is stablecoin infrastructure